Term Life Insurance

What is Term Life Insurance?

Term life insurance is a type of life insurance policy that provides coverage for a specified period, or "term," such as 10, 20, or 30 years. If the insured person dies during the term, the policy pays a death benefit to the beneficiaries. If the term expires and the policyholder is still alive, the coverage ends without any payout.

Term life insurance is typically more affordable than permanent life insurance and is often used to provide financial protection during the years when income replacement is most needed, such as when raising children or paying off a mortgage.

Key features of Term include:

1. Fixed Term: Coverage lasts for a specific period, typically 10, 20, or 30 years.

2. Affordable Premiums: Generally lower premiums compared to permanent life insurance.

3. Death Benefit: Pays a lump sum to beneficiaries if the insured dies during the term.

4. No Cash Value: Unlike permanent life insurance, term policies do not build cash value and only provide death benefits.

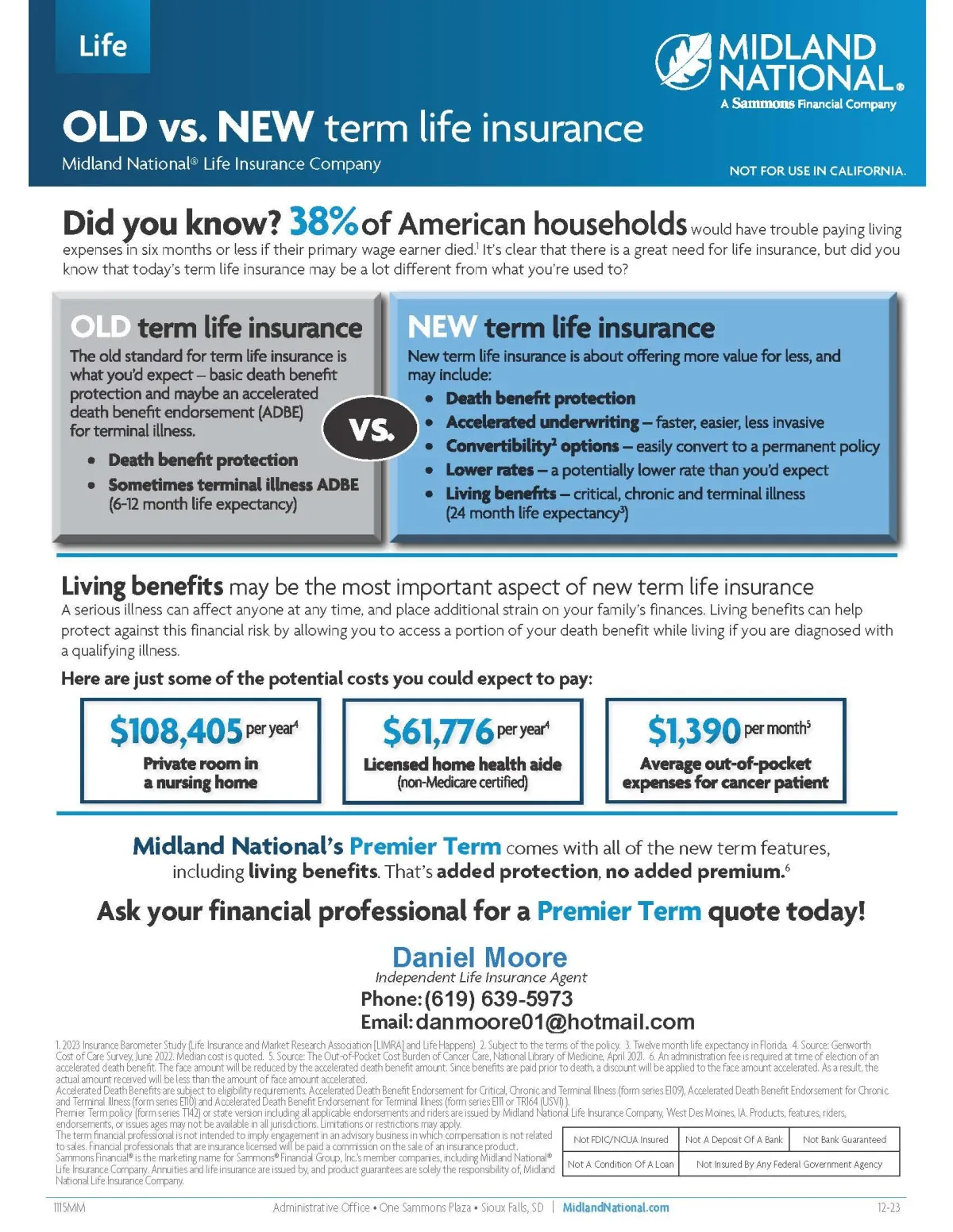

Old Vs. New Term Life Insurance

Old Term Life Insurance: Basic death benefit protection

Terminal illness accelerated death benefit endorsement (ADBE) with 6-12 month life expectancy

New Term Life Insurance: Enhanced death benefit protection

Accelerated underwriting for easier, faster, less invasive processing

Convertibility options to switch to a permanent policy

Potentially lower rates

Living benefits for critical, chronic, and terminal illnesses with 24-month life expectancy

Living Benefits: Highlighted as the most important aspect, offering financial protection against serious illness by accessing part of the death benefit early.

Cost Estimates: Private room in a nursing home: $108,405 per year

Licensed home health aide: $61,776 per year

Average out-of-pocket expenses for cancer patients: $1,390 per month

Midland National’s Premier Term: Includes all new features for added protection.

CUSTOMER CARE

(951) 561-3676

25920 Iris Ave Ste 13A Box612

Moreno Valley, CA 92551

LEGAL

FOLLOW US

Insurance products offered through CDM Insurance Solutions (CDM Business Group LLC), License #6005408 © 2024 Veterans Legacy Center All rights reserved.