Indexed Universal Life Insurance for Veterans

What is Indexed Universal Life Insurance?

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that offers a death benefit along with a cash value component. The cash value grows based on the performance of a market index, such as the S&P 500, which allows for potential higher returns compared to traditional universal life insurance.

Key features of IUL's include:

1. Flexible Premiums: Policyholders can adjust their premium payments within certain limits.

2. Death Benefit: Provides a tax-free death benefit to beneficiaries.

3. Cash Value Growth: The cash value can grow based on index performance, with a cap on maximum returns and typically a floor to protect against market losses.

4. Loans and Withdrawals: Policyholders can borrow against or withdraw from the cash value typically tax-free.

IUL policies combine the protection of life insurance with the growth potential linked to market indices, making them an attractive option for those looking for both insurance coverage and investment opportunities.

How an Indexed Account Works

Death Benefit Protection: Provides a death benefit alongside potential cash value growth.

Index Account Mechanics: Interest is credited based on the performance of a financial index, with a minimum interest rate of zero (the floor) and a cap on maximum growth.

Market Independence: The policy money is not directly invested in any index or stock market.

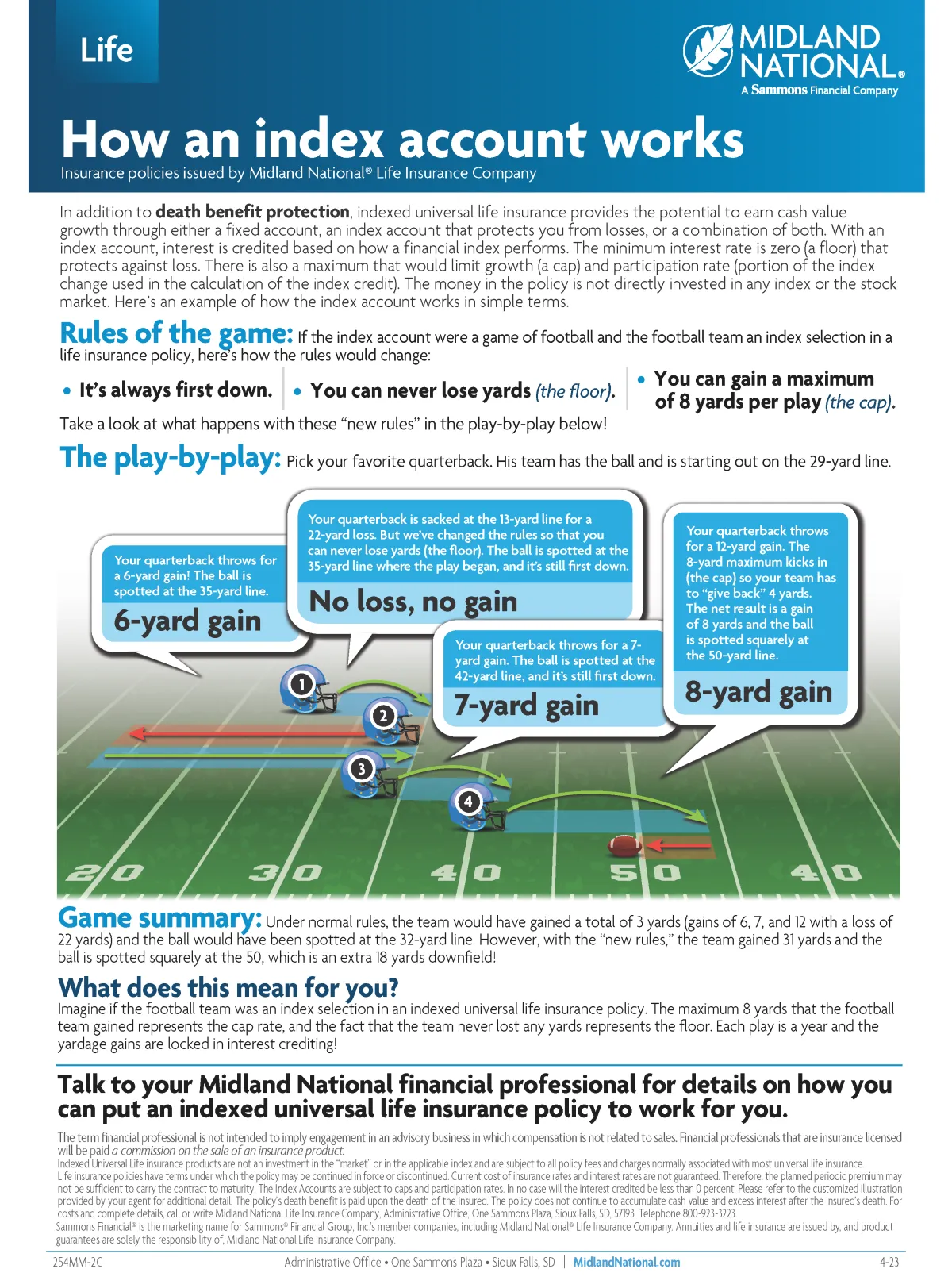

Rules of the Game:

It's always first down.

You can never lose yards (the floor).

You can gain a maximum of 8 yards per play (the cap).

Play-by-Play Examples:

A 6-yard gain moves the ball to the 35-yard line.

No loss or gain when sacked at the 13-yard line; ball remains at the 35-yard line.

A 7-yard gain moves the ball to the 42-yard line.

A 12-yard gain, reduced to 8 yards due to the cap, places the ball at the 50-yard line.

Game Summary: With the new rules, the team gains 31 yards, representing an 18-yard improvement over normal rules.

Implications: Indexed universal life insurance ensures no loss of principal (floor) and limits gains to the cap, locking in interest credits.

Accelerated Death Benefits

Critical Illness: conditions that may qualify include heart attack, cancer, stroke, major organ transplant, and kidney failure.

Chronic Illness: unable to perform at least two activities of daily living (bathing, continence, dressing, eating, toileting, and transferring) for at least 90 days.

Terminal Illness: diagnosed medical condition that results in a life expectancy of 24 months or less.

Is Indexed Universal Life Insurance a Fit for You?

Indexed Universal Life Insurance is designed for long-term planning—not low monthly premiums.

As a general guideline:

Ages 20-29: Often $200–$300/month

Ages 30–39: often $300–$500/month

Ages 40–49: often $400–$700/month

Ages 50–59: often $600–$1,000+/month

Ages 60+: usually not ideal for IUL

These are not quotes, but realistic funding ranges.

If those ranges feel uncomfortable, we also help with Term Life and Final Expense options.

Request Information About Indexed Universal Life Insurance for Veterans & Their Spouses

Before submitting your request, please confirm the information below. This helps ensure we can provide accurate guidance and respect your time.

CUSTOMER CARE

(951) 561-3676

25920 Iris Ave Ste 13A Box612

Moreno Valley, CA 92551

LEGAL

FOLLOW US

Insurance products offered through CDM Insurance Solutions (CDM Business Group LLC), License #6005408 © 2024 Veterans Legacy Center All rights reserved.