WELCOME TO MEDICARE 101 For Veterans

What is Medicare?

Medicare is a federal health insurance program primarily designed for individuals aged 65 and older, but it also covers younger people with certain disabilities and patients with End-Stage Renal Disease (ESRD).

For veterans, it's important to understand how Medicare works alongside benefits provided by the Veterans Health Administration (VHA). Many veterans choose to enroll in Medicare to ensure they have health coverage outside the VA system. Enrolling in Medicare can provide additional options and flexibility, as it allows veterans to receive treatment from non-VA healthcare providers without requiring VA authorization. This can be particularly beneficial for veterans living in areas where VA facilities are not easily accessible or for those seeking care that may be limited at VA facilities.

Moreover, having Medicare can be a safety net for veterans who might lose their VA health benefits due to changes in their health coverage eligibility. While VA health coverage is typically quite comprehensive, having Medicare means not having to rely solely on VA hospitals and clinics and helps avoid any potential gaps in coverage.

It's also crucial for veterans to understand how to coordinate these benefits effectively to maximize their healthcare options while minimizing out-of-pocket costs. For example, Medicare Part B may cover services that the VA does not, and enrolling in Medicare can prevent penalties that are associated with late enrollment if a veteran decides to use Medicare benefits later in life.

The Different Parts of Medicare

Medicare Part A

(Hospital Insurance)

Medicare Part B

(Medical Insurance)

Medicare Part C

(Medicare Advantage)

Medicare Part D

(Prescription Drug)

Medicare Part D

(Prescription Drug)

🛌🏽Medicare Part A

Hospital Insurance

Part A helps pay for covered hospital stays and most of the inpatient services

Coverage includes:

A semi-private room

Your hospital meals

Skilled nursing services

Care in special units, such as intensive care

Drugs, medical supplies and medical equipment used during an inpatient stay

Lab tests, X-rays and medical equipment as an inpatient

Operating room and recover room services

Some blood transfusions in a hospital or skilled nursing facility

Inpatient or outpatient rehabilitation services after a qualified inpatient stay

Part-time, skilled care for the homebound after a qualified inpatient stay

Hospice care for the terminally ill, including medications to manage symptoms and control pain

Part B helps pay for covered care at a clinic or at a hospital as an outpatient

Coverage includes:

Licensed provider visits, including in the hospital

Annual wellness Visit

Ambulatory Surgery Center (ASC) services

Ambulance and emergency room services

Skilled nursing services

Preventive services, such as flu shots or mammograms

Clinical laboratory services, such as blood and urine tests

X-rays, MRIs, CT scans, EKGs, and some other diagnostic tests

Some health programs, such as smoking cessation, obesity counseling and cardiac rehab

Physical therapy, occupational therapy and speech-language pathology services

Diabetes screenings, diabetes education and certain diabetes supplies

Mental health care

Durable medical equipment for use at home, such as wheelchairs and walkers

Telehealth visits

🩺Medicare Part B

Medical Insurance

🩺🛌🏽Medicare Part C

Medicare Advantage plans combine Part A and part B benefits

Medicare advantage plans are offered by private insurance companies approved for Medicare. In addition to Part A and part B benefits, many plans offer:

💊 Part D prescription drug coverage

🦻🏽 Routine hearing exams and hearing aids

🦷 Routine dental care

👓 Routine eye exams, eyeglasses or contact lenses

💪🏽 Wellness benefits such as gym memberships

🚌 Benefits vary by plan and could include other extra benefits such as transportation to medical appointments and credits to buy health products

Medicare Part D provides coverage for prescriptions and some vaccines

Coverage includes:

Drugs most commonly prescribed for Medicare beneficiaries as determined by federal standards

Specific brand name drugs and generic drugs included in the plan's formulary (list of covered drugs)

Commercially available vaccines not covered by Part B

Part D plan typically does not cover:

• Drugs not listed on a plan’s formulary

• Drugs prescribed for anorexia, with loss or weight gain

• Prescriptions for fertility and sexual or erectile dysfunction (ED)

• Prescriptions for cosmetic purposes or hair growth

• Prescription vitamins and minerals

• Non-prescription drugs (e.g. over-the-counter medications)

💊Medicare Part D

Prescription Drugs

☂️Medigap

Plans are offered by private insurance companies but are standardized by the federal government

Medicare supplement insurance (Medigap) plans can help pay some of the out-of-pocket costs not paid by Parts A & B

All include full or partial coverage for:

Part A hospital coinsurance

Part B coinsurance or copays

Costs of blood transfusions (first 3 pints)

Costs for 365 extra hospital days

Hospice care coinsurance

Some may also help pay for:

Part A deductible

Part B deductible

Foreign travel emergency care up to plan limits

Part A skilled nursing facility care coinsurance

How Do Medicare and VA Benefits Work Together?

Many veterans wonder whether they need Medicare if they already receive health care through the Department of Veterans Affairs (VA). The answer depends on your individual situation, but it's important to understand that Medicare and VA benefits are separate programs.

VA health care generally covers services received at VA facilities and through approved VA community care providers. Medicare typically covers services received outside of the VA system from Medicare-approved doctors, hospitals, and other healthcare providers.

Because the two programs do not automatically coordinate benefits, many veterans choose to enroll in Medicare Part B when they become eligible. Having both VA health care and Medicare may provide greater flexibility and access to care.

✔ Access to non-VA doctors and hospitals

✔ Coverage when traveling outside their local VA network

✔ Additional healthcare options and provider choice

✔ Protection against future late enrollment penalties

Can Veterans Have Both VA Benefits and Medicare?

Yes. Many veterans have both VA health care and Medicare. In fact, Medicare can complement VA benefits by providing coverage for services received outside of the VA healthcare system.

What About Dental Coverage?

VA dental benefits are only available to certain eligible veterans, and Original Medicare generally does not cover routine dental care. As a result, some veterans explore Medicare Advantage plans with dental benefits or standalone dental insurance plans to help fill potential gaps in coverage.

Learn More:

Official VA Resource: VA Health Care and Other Insurance

Original Medicare vs Medicare Advantage

Benefits, costs, provider networks, and coverage vary by plan and location. Review plan details carefully before enrolling.

Which Option Is Right for Veterans?

Many veterans choose Medicare Advantage plans because of the additional dental, vision, hearing, prescription drug benefits, OTC allowances, and Part B Premium givebacks while others prefer Original Medicare with a supplement for provider flexibility.

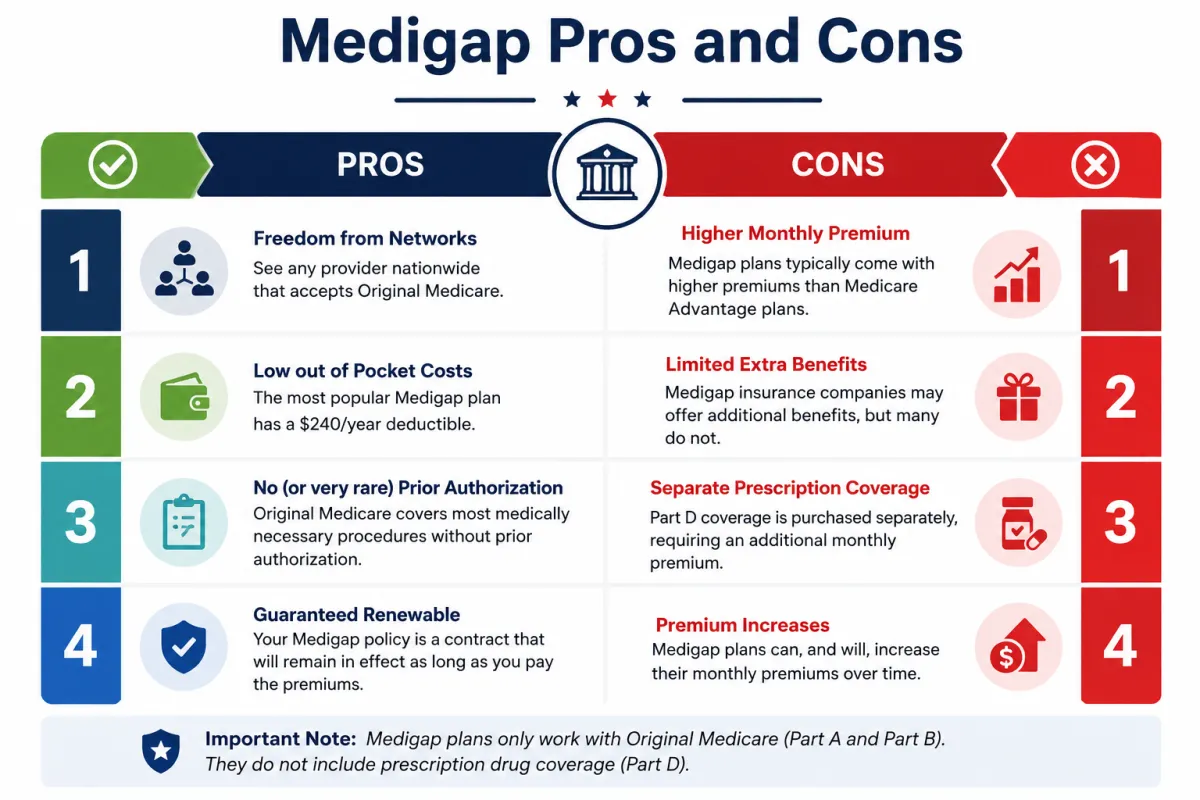

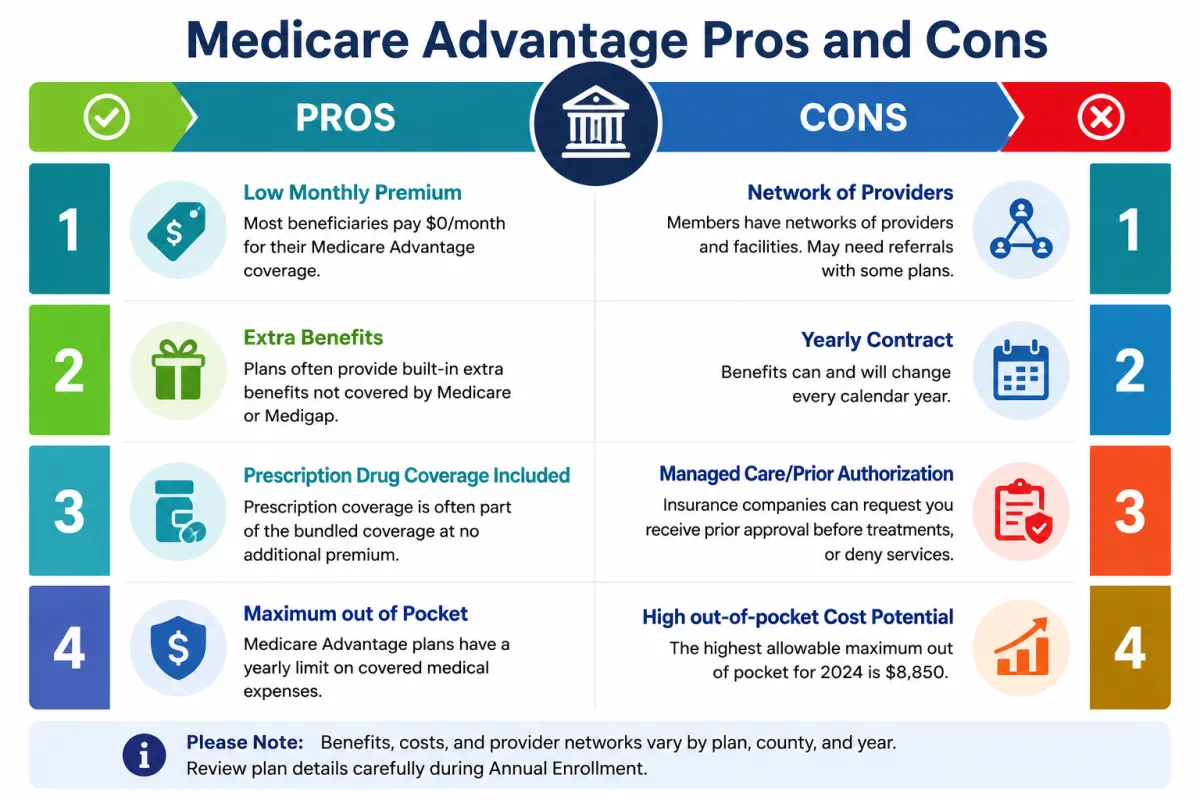

The Pros & Cons of Medigap & Medicare Advantage Plans

When you're ready to choose a Medicare plan, you'll have two primary options to consider: Medigap (also known as Medicare Supplement Plans) and Medicare Advantage Plans. Medigap plans work alongside your original Medicare coverage to help cover additional costs, such as deductibles, copayments, and coinsurance. On the other hand, Medicare Advantage Plans, offered by private insurance companies, provide all your Part A and Part B benefits and often include additional services like prescription drug coverage, dental, and vision care. Each option offers distinct benefits and costs, allowing you to select the plan that best suits your healthcare needs and financial situation.

FAQs

What are the different parts of Medicare?

Medicare is divided into four parts: Part A (Hospital Insurance), which covers inpatient hospital stays and skilled nursing facility care; Part B (Medical Insurance), which covers outpatient services, such as doctor visits and preventive services; Part C (Medicare Advantage), an alternative to Original Medicare that often includes additional benefits like dental, vision, and hearing; and Part D (Prescription Drug Coverage), which covers the costs of prescription medications.

When can I enroll in Medicare?

You can enroll in Medicare during the Initial Enrollment Period, which begins three months before you turn 65 and ends three months after your 65th birthday. There are also Special Enrollment Periods for those who may be covered by a current employer’s health plan beyond age 65, and a General Enrollment Period from January 1 to March 31 each year if you missed your Initial Enrollment.

Do I need Medicare if I’m still working and have employer health insurance?

You may not need to sign up for Medicare at 65 if you have health insurance through your employer. However, it is important to sign up for Medicare Part A, which is premium-free for most people, as it may cover some costs not included in your employer's plan. Consult with your HR department or a Medicare advisor to understand how your current insurance works with Medicare.

What does Medicare not cover?

Medicare does not cover everything. Items and services not covered include long-term care, most dental care, eye examinations related to prescribing glasses, dentures, cosmetic surgery, acupuncture, hearing aids and exams for fitting them, and routine foot care.

How much does Medicare cost?

The cost of Medicare varies based on the coverage you choose. Part A is usually free if you or your spouse paid Medicare taxes for a certain amount of time. Part B has a standard monthly premium of $174.70 in 2024, which could be higher based on your income. Medicare Advantage Plans (Part C) and Prescription Drug Plans (Part D) premiums vary by plan. Additionally, there may be deductibles and co-pays depending on the services used.

Can I change my Medicare coverage?

Yes, you can change your Medicare coverage during specific times of the year. The Annual Enrollment Period from October 15 to December 7 allows you to change, add, or drop Medicare health or drug plans, with changes effective the following January 1. Also, the Medicare Advantage Open Enrollment Period from January 1 to March 31 each year allows anyone with a Medicare Advantage Plan to switch to a different Medicare Advantage Plan or switch back to Original Medicare.

Are you already getting benefits from Social Security or the Railroad Retirement Board (RRB)?

In most cases, you’ll automatically get Part A and Part B starting the first day of the month you turn 65. If your birthday is on the first day of the month, Part A and Part B will start the first day of the prior month.

Are you under 65 and disabled?

You automatically get Part A and Part B after you get disability benefits from Social Security or certain disability benefits from the RRB for 24 months.

Do you have ALS (Amyotrophic Lateral Sclerosis, also called Lou Gehrig’s disease)?

You automatically get Part A and Part B the month your disability benefits begin.

I have good coverage at VA, should I enroll into a Medicare Advantage Plan?

Depending on the plan in the area, you can address the benefits we have in a Medicare Advantage (MA) or Medicare Advantage Prescription Drug (MAPD) plan.

Are you worried you may lose some of your VA benefits by enrolling in an MA or MA-PD plan?

VA and MA plan benefits are separate; therefore, it is not possible to lose VA benefits by enrolling in an MA or MA-PD plan. It does not affect the consumer’s eligibility for VA care.

Are you sure that your health benefits with the VA will remain the same for as long as you will need them?

This may not be true. For some of the higher medal awardees and disability ratings, this may be true, but generally is not true for the majority of veterans.

Are my VA health benefits guaranteed or set in stone?

The answer is no. Congress mandates budgeting for the VA, which impacts benefits for veterans, and these could change at any time. Veterans would be notified of any changes in writing.

What is the value of enrolling into Medicare Part A and B and having VA health care?

More choices, more opportunities for second opinions, possibly see a provider quicker, and benefits outside of the area that have VA facilities.

Social Security said I would have to pay a late Part B Penalty, why?

Special Enrollment Periods under Part A & Part B do exist. The consumer must contact Social Security to ask for this Special Enrollment Period. The SEP Starts: Once Social Security decides they qualify for a Special Enrollment Period and Ends: At least 6 months later. Coverage starts the month after they sign up.

Our Carriers

CUSTOMER CARE

(951) 561-3676

25920 Iris Ave Ste 13A Box612

Moreno Valley, CA 92551

LEGAL

FOLLOW US

Insurance products offered through CDM Insurance Solutions (CDM Business Group LLC), License #6005408 © 2024 Veterans Legacy Center All rights reserved.